Introduction

If you are a non-U.S. founder, chances are you’ve heard this advice before: “Just get an EIN and you can open a U.S. bank account.”

For years, that idea circulated in Facebook groups, YouTube videos, and freelancer forums. Many international entrepreneurs followed it, expecting smooth U.S. banking access only to face rejections, frozen applications, or endless compliance requests.

In 2026, this confusion has become even more costly.

U.S. banks have tightened their rules. Fintech platforms are more cautious. Compliance checks are deeper, slower, and far less forgiving especially for non-residents.

So here’s the real question every international founder must answer before applying for banking:

Is having an EIN alone truly enough to open and maintain an LLC bank account in 2026 or are you missing something critical?

Quick Direct Answer

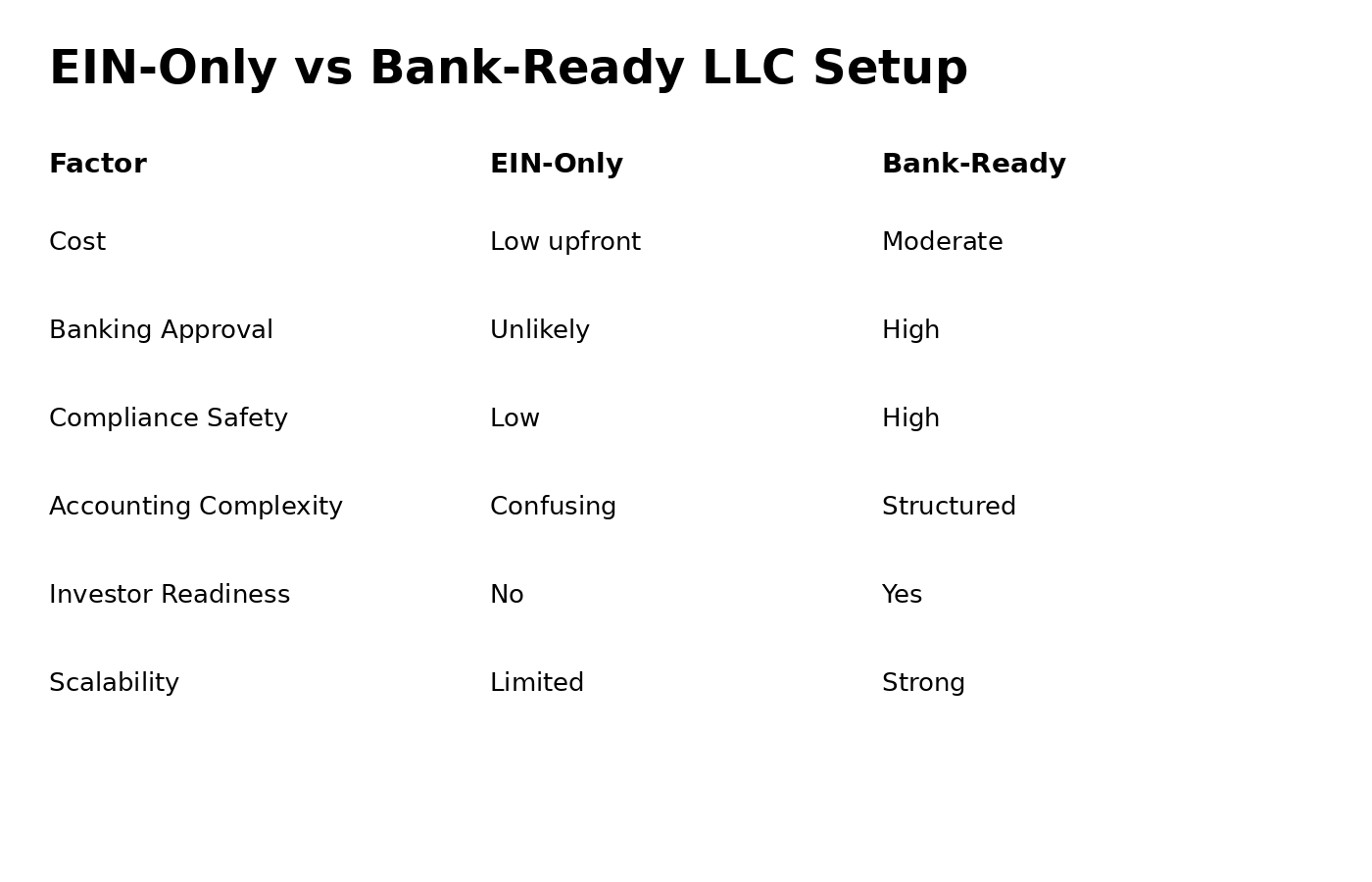

❌ No an EIN alone is not enough for LLC banking in 2026.

An EIN is only a tax identification number. Banks now require entity verification, ownership transparency, and operational proof before approving accounts especially for non-U.S. residents.

⚠️ Caution: Many founders get an EIN successfully but fail at the banking stage, wasting time and risking compliance issues.

Explanation of Legal Possibilities

What an EIN Actually Does

An EIN (Employer Identification Number) is issued by the IRS. Its purpose is simple:

- Identify your LLC for tax reporting

- Allow the IRS to track income and filings

- Enable hiring employees (if applicable)

That’s it.

An EIN does not:

- Prove your business is operational

- Verify who controls the company

- Satisfy anti-money laundering (AML) rules

- Replace identity or compliance documentation

Think of the EIN as a starting key, not the engine.

What Banks Really Require in 2026

By 2026, most U.S. banks and fintechs follow stricter KYC (Know Your Customer) and AML rules. For non-U.S. founders, this usually includes:

- Approved LLC formation documents

- EIN confirmation letter (CP 575)

- Operating Agreement

- Ownership disclosure (BOI-aligned)

- Valid passport of owners

- U.S. business address (not virtual-only in many cases)

- Proof of business activity (contracts, invoices, website)

- In some cases: ITIN or U.S. tax presence indicators

Without these, an EIN alone means very little to a bank.

Single-Member vs. Multi-Member LLC Reality

Single-Member LLCs (Non-Resident):

- Higher scrutiny

- Often flagged as “pass-through risk”

- More likely to require ITIN or additional verification

Multi-Member LLCs:

- Slightly easier if members are transparent

- Still require full documentation

- EIN alone still insufficient

In both cases, the EIN is necessary but never sufficient.

Advantages / Pros

Why Founders Think EIN Is Enough

Many international founders consider an EIN-only approach because:

- Fast to obtain

- Low upfront cost

- Marketed aggressively online

- Sounds “official” and government-issued

Common perceived benefits:

- ✔ Appears compliant at first glance

- ✔ Required step for any U.S. company

- ✔ Feels like progress

But these advantages disappear the moment banking begins.

Risks / Cons

1. Bank Account Rejection

What it is:

Your application is declined after submission.

Why it matters:

You lose weeks and may be flagged internally.

Example:

A founder from Pakistan gets an EIN, applies to Mercury, and is rejected due to missing operating proof.

2. Frozen or Closed Accounts

What it is:

Account opens, then gets restricted.

Why it matters:

Funds can be held for months.

Example:

A Stripe Atlas-style setup opens briefly, then freezes after compliance review.

3. Compliance Red Flags

What it is:

Incomplete documentation triggers AML alerts.

Why it matters:

Future banking becomes harder.

Example:

Applying to multiple banks with the same EIN causes internal risk tagging.

4. Tax & Reporting Confusion

What it is:

EIN without proper structure leads to filing mistakes.

Why it matters:

Penalties and IRS notices.

Example:

Founder misses BOI filing or Form 5472 due to lack of guidance.

When EIN-Only Setups Make Sense

An EIN-only approach may work temporarily if:

- You are not opening a bank account yet

- You are preparing documents in parallel

- You are in early planning stage

- No payments will be processed immediately

Checklist:

- ☐ No incoming revenue yet

- ☐ No payment processors required

- ☐ Short-term placeholder only

This is a transition phase, not a final setup.

When a Full Compliance Setup Is Better

A complete, bank-ready structure is better if:

- You plan to accept payments

- You want Stripe, PayPal, Wise, Mercury

- You work with U.S. or EU clients

- You want long-term stability

- You want to avoid rejections

This approach prioritizes:

- Risk reduction

- Faster approvals

- Long-term scalability

Alternative Structure: Using a Banking-Friendly Operating Model

Some founders use a compliance-first LLC structure, where banking readiness is prioritized from day one.

What it is:

- Proper operating agreement

- Transparent ownership

- Correct tax classification

- Activity proof prepared in advance

Benefits:

- Faster bank approval

- Lower freeze risk

- Cleaner accounting

Downsides:

- Higher initial cost

- Requires planning and guidance

This is often the smartest route for serious founders.

Real-Life Case Study

Founder: Ali, from Pakistan

Business: SaaS subscription services

Initial Decision:

Ali obtained an EIN and assumed banking would be easy.

Problem Faced:

Three fintech rejections due to lack of operating proof and unclear tax setup.

Solution:

He restructured his LLC with:

- Updated operating agreement

- ITIN application

- Clear business activity documentation

Result:

Approved by a U.S. fintech within 10 days, with stable banking since.

Frequently Asked Questions (FAQs)

Q1: Can I open a U.S. bank account with just an EIN?

No. Most banks require full entity and owner verification.

Q2: Do I need an ITIN for banking?

Not always, but it significantly improves approval chances.

Q3: Are fintech banks easier than traditional banks?

Sometimes but their compliance rules are now very strict.

Q4: Is EIN useless then?

No. It’s essential but incomplete on its own.

Q5: Can I fix a rejected application?

Yes, but reapplying without fixing structure can make things worse.

Conclusion

In 2026, it depends but leaning on an EIN alone is no longer smart.

Use this logic:

- EIN = starting requirement

- Banking = compliance + proof + structure

If you only need an EIN for planning, that’s fine.

If you want real banking, payments, and growth you need more.

Clarity comes from preparation, not shortcuts.

Call to Action

If you’re a non-U.S. founder and want to open a bank-ready U.S. LLC without rejections or freezes, our team helps you do it the right way from EIN to compliance-ready banking.

We focus on:

- Correct structure

- Banking approval strategy

- Long-term stability

👉 Book a consultation or contact us today to avoid costly mistakes and build with confidence.